If you’ve tuned into the news lately, you’ve probably heard a lot of talking heads shouting about "The Fed," "Interest Rates," and "Inflation." It sounds like a bunch of academic jargon designed to make your eyes glaze over, but here at Regular Guy Economics, we like to peel back the curtain.

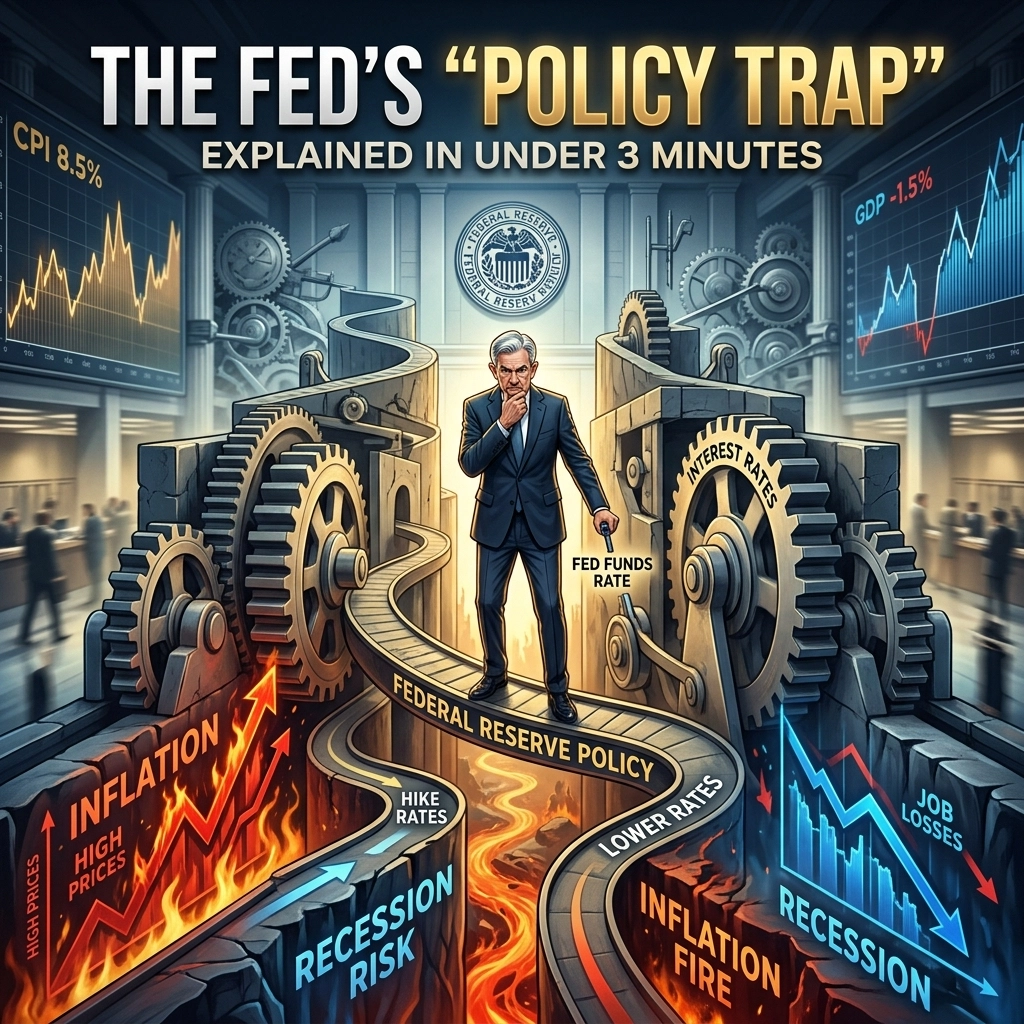

The truth is, the Federal Reserve: our nation’s central bank: is currently stuck in what economists call a "Policy Trap." Think of it like being stuck between a rock and a hard place, except the rock is a total economic collapse and the hard place is your grocery bill doubling every six months.

Let’s break down how they got here, why they can’t seem to get out, and what it means for your wallet.

The Adrenaline Shot That Never Stopped

To understand the trap, we have to go back to 2008. Remember the Great Financial Crisis? The world’s economy was basically on life support. To keep the heart beating, the Fed did something drastic. They dropped interest rates to near zero and started printing money to buy up bonds: a fancy move called "Quantitative Easing" (QE).

It was supposed to be a temporary shot of adrenaline. The idea was simple: make borrowing money so cheap that businesses would expand, people would buy houses, and the economy would roar back to life.

And it worked! Sort of.

The problem is that once you give a patient a powerful drug to save their life, it’s really hard to take them off it. The Fed kept rates low for a decade. They turned the "emergency" settings into the "new normal." By doing this, they created a generation of investors and companies that only know how to survive on cheap, easy money.

The "Wealth Effect" Addiction

Here is where the trap really starts to snap shut. By keeping rates at zero and pumping trillions of dollars into the system, the Fed didn’t just help the local bakery stay open. They accidentally (or intentionally, depending on who you ask) inflated the biggest asset bubbles in human history.

When money is free, it has to go somewhere. It went into the stock market. It went into real estate. It went into crypto. This created something called the "Wealth Effect." When your 401(k) looks huge and your house value doubles, you feel rich. When you feel rich, you spend money. When you spend money, the economy looks great on paper.

But according to the research, the Fed has now become a "prisoner to the financial markets it supports." They’ve spent fifteen years making sure the stock market goes up. Now, if they try to raise interest rates to a "normal" level, the stock market throws a temper tantrum.

If the market drops 20% or 30%, people stop feeling wealthy. They stop spending. Businesses start laying people off. Suddenly, the Fed is looking at a recession they caused. So, they get scared, they lower rates again, and the cycle continues. They are trapped by the very success of their own intervention.

The New Villain: Sticky Inflation

For a long time, the Fed could get away with this. They kept rates low, the markets went up, and inflation stayed quiet. It was the "Goldilocks" economy: not too hot, not too cold.

Then 2020 happened. Then 2021. Then 2022.

Between supply chain meltdowns and the government printing even more money to handle the pandemic, inflation finally woke up from its long nap. Suddenly, the cost of eggs, gas, and rent started screaming higher.

This changed the game. Usually, when the stock market dips, the Fed just lowers rates to save the day. But they can’t do that anymore. If they lower rates to save the stock market, they risk making inflation even worse. If inflation hits 8%, 9%, or 10%, the "Regular Guy" can’t afford to live.

Why They Can't Move Rates Right Now

So, why are they "trapped" specifically right now, in April 2026?

Imagine you’re driving a car toward a cliff. That cliff is a massive recession. You want to hit the brakes (raise interest rates) to slow down and avoid inflation. But your brakes are connected to a bomb. If you press them too hard, the bomb (the $34 trillion in national debt and the fragile banking system) explodes.

If the Fed raises rates to 6% or 7% to really kill inflation, the interest the government has to pay on our national debt becomes so high that we can’t afford anything else. Also, your neighbor who just got a 7% mortgage might default, and the bank that holds that mortgage might go bust.

On the flip side, if the Fed cuts rates back to 2% to help the housing market and the stock market, inflation will likely come roaring back. We’d be right back to $7 a gallon for gas.

They are stuck in a "Policy Trap" because every move they make has a devastating side effect. They are trying to find a "Soft Landing," which is economic speak for "landing a jumbo jet on a postage stamp during a hurricane without spilling anyone's coffee."

The Broken Compass

One of the biggest issues is that the Fed’s tools were designed for a different era. They use interest rates like a giant thermostat for the whole country. But the country isn't one room.

When they raise rates, it might hurt a young family trying to buy their first home, but it doesn't really stop a multi-billion dollar tech company with a mountain of cash from spending. It’s a blunt instrument used on a very delicate situation.

Furthermore, as the research suggests, the Fed is fixated on "financial-market feedback." They spend more time looking at what Wall Street traders think than what is happening at your local grocery store. Because they are so afraid of a market crash, they wait too long to act, and when they do act, they have to do it so aggressively that it breaks something.

What This Means for You

So, what’s a regular guy supposed to do while the geniuses at the Fed try to wiggle out of this trap?

First, realize that the era of "easy money" is likely over, even if they cut rates a little bit. The days of 2% mortgages are probably in the rearview mirror for a long time.

Second, understand that volatility is the new normal. Because the Fed is trapped, they are going to be hesitant. They will say one thing on Tuesday and another on Thursday. The markets will swing wildly based on every single word that comes out of Chairman Powell’s mouth.

Finally, keep an eye on your own "personal economy." In a policy trap, the Fed isn't coming to save you. They are too busy trying to save themselves from the mess they spent the last 15 years making.

The Fed’s "Policy Trap" is essentially a debt trap. We’ve borrowed from the future to make the present look better, and now the bill is coming due. Whether they choose to pay that bill with a recession or with more inflation remains to be seen, but one thing is for sure: there is no "get out of jail free" card this time.

The "Policy Trap" isn't just an abstract concept for billionaires and bankers. It’s the reason your savings account finally earns a little interest, but also the reason your car loan is twice as expensive as it used to be. It’s the tension that defines our current world.

As we watch this unfold, remember that the "experts" are often just guessing as much as we are: they just have better-looking charts.

Be mindful, be watchful and good luck.