The experts are popping champagne. Inflation dropped to 2.4% in January 2026, down from 2.7% in December. The Federal Reserve is practically doing a victory lap, telling us we're "almost there" to their magical 2% target. Core inflation? Down to 2.5%, the lowest since March 2021.

So why does your wallet feel like it's been mugged?

Here's the uncomfortable truth: the official inflation numbers and the reality of your daily expenses are living in two completely different universes. While the government pats itself on the back, your car insurance premium just went up 30%, your grocery bill looks like a small mortgage payment, and don't even get me started on what's happening with housing costs.

The Magic Basket Trick

Let's talk about how the Consumer Price Index (CPI) actually works, because it's basically a magic show. The government creates a "basket of goods" that's supposed to represent what Americans buy. Sounds reasonable, right? Except they get to decide what goes in that basket, how much weight each item gets, and, here's the kicker, they change the basket whenever it's convenient.

Think of it like this: if steak prices go through the roof, they assume you'll switch to hamburger. If hamburger gets too expensive, well, maybe you'll eat chicken. And if chicken prices soar? They figure you'll adjust your "preferences" accordingly. This isn't inflation measurement, it's a choose-your-own-adventure book where the ending is always "inflation isn't that bad."

This sleight of hand is called "substitution," and it's one of several tricks that make the CPI look better than your actual experience. They also use something called "hedonics", the idea that if your laptop is faster than last year's model, even if it costs more, that's not really inflation because you're getting "more value." Try explaining that logic to your credit card bill.

What They're Not Counting

The official numbers look rosy partly because they're conveniently ignoring or downplaying the expenses that are absolutely demolishing household budgets.

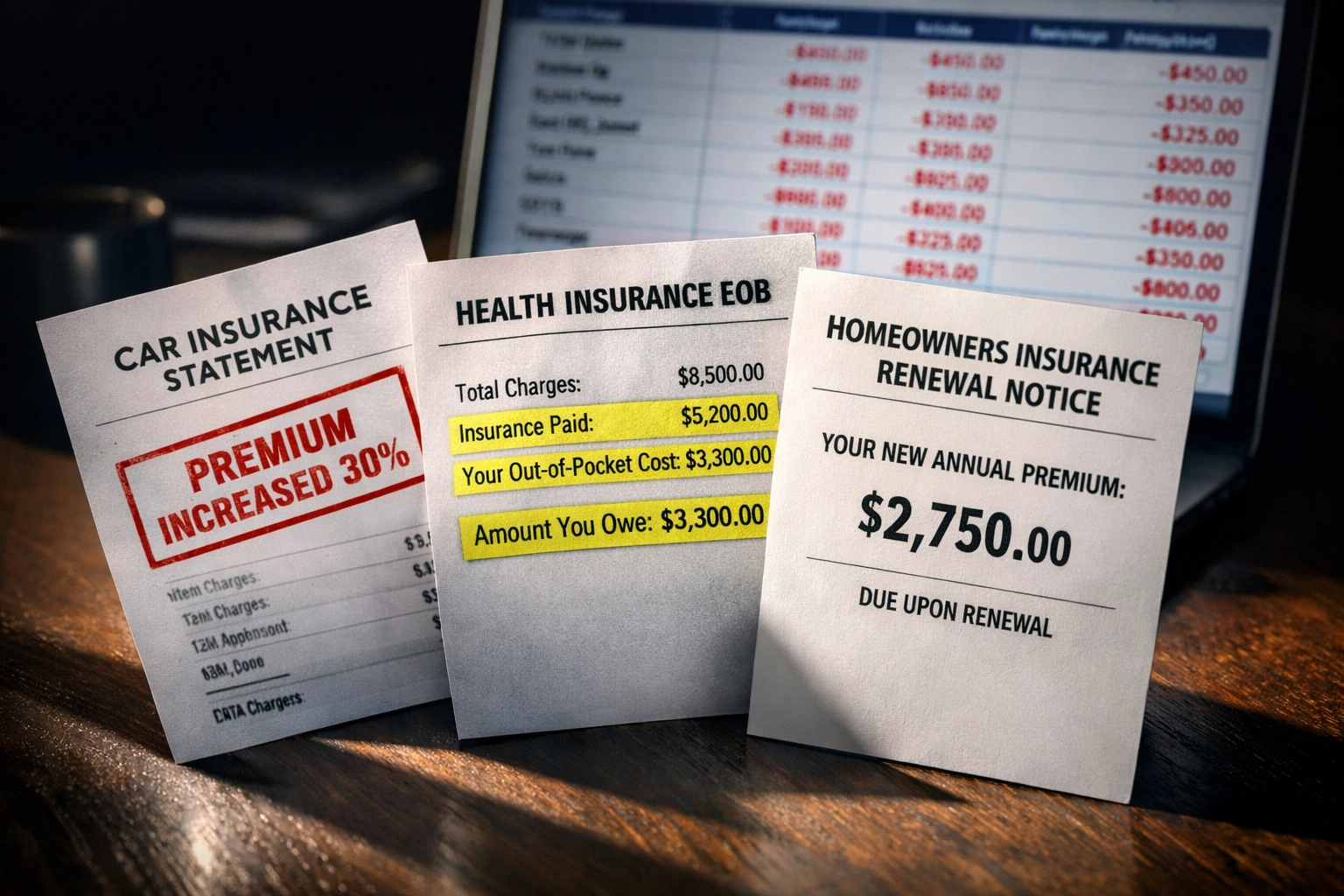

Insurance Premiums: The Silent Budget Killer

Car insurance has become a second car payment for many families. Premiums have skyrocketed 20-30% in many states over the past two years, but this barely registers in the CPI calculation because insurance is weighted much lower than what you actually spend. Homeowners insurance? Same story. If you live in Florida or California, you might not even be able to get coverage anymore, or you're paying double what you paid three years ago.

Health insurance premiums and out-of-pocket costs continue their relentless climb upward, but the CPI treats healthcare as just another line item, not the budget-crushing monster it's become. When your employer shifts more costs onto you through higher deductibles and co-pays, that's invisible to the official inflation metrics.

The Grocery Store Reality Check

Walk into any grocery store and play a game: find something that costs the same as it did two years ago. Eggs were the poster child for inflation a couple years back, and while they've come down from their peak, they're still way higher than pre-2021 levels. But here's what's really insane: everything else quietly went up while we were distracted by egg prices.

A pound of ground beef that cost $4 in 2021 is now $7 or $8. Chicken breast? Up 40-50% in many markets. A box of cereal that was $3.50 is now $5.50, and they shrunk the box. This is "shrinkflation," where you get less product for the same price, and it's everywhere. That bag of chips is more air than potato now, and your ice cream container has a weird concave bottom that hides how little is actually in there.

The CPI captures some of this, but not the full psychological gut-punch of watching your $150 grocery run turn into $250 for the same cart of food.

Housing: The Elephant in Every Room

Here's where the official numbers become almost comical. The CPI measures housing costs primarily through "Owner's Equivalent Rent", basically asking homeowners what they think they could rent their house for. This creates a lag of months or even years before real housing market changes show up in inflation numbers.

If you're actually trying to buy a house right now, you're dealing with prices that are still 40-50% higher than they were four years ago in many markets, combined with mortgage rates that are triple what they were. That's not a 2.4% inflation environment, that's a "you're permanently priced out" environment.

Renters aren't doing much better. While rent growth has slowed in some markets, you're still paying 25-30% more than you were a few years ago, and that's assuming you could even find a place. The official numbers say rent inflation is "moderating." Try telling that to someone paying $2,200 for a one-bedroom apartment that cost $1,600 three years ago.

What's Really Happening Behind the Curtain

So if the official numbers say inflation is under control, but your lived experience says otherwise, what's actually going on?

Some economists, the ones not on the government payroll, are waving red flags. The Peterson Institute for International Economics is predicting inflation could hit 4% or higher by the end of 2026. Why? Because all the factors that caused inflation in the first place haven't actually gone away; they've just been temporarily masked.

The Tariff Time Bomb

Remember all those tariffs that got slapped on imports? Companies initially absorbed those costs by using up inventory they'd already purchased at lower prices. But that buffer is running out. Now businesses are passing those costs to consumers in small, steady increments that don't trigger sticker shock but add up over time. By mid-2026, we'll likely see the full impact hit your wallet.

The Government Spending Party Continues

The federal deficit might exceed 7% of GDP in 2026. That's not "fiscal responsibility", that's a spending binge. When the government pumps that much money into the economy, it doesn't just disappear. It shows up as demand for goods and services, which pushes prices up. Politicians love to hand out money (potential tariff dividend checks, extended subsidies), but that money has to come from somewhere, and it usually comes from your purchasing power.

The Labor Market Squeeze

With tighter immigration policies restricting labor supply, businesses are struggling to find workers. That means wages have to go up to attract talent, which is good for workers but gets passed through to consumers as higher prices. It's not inflation in the traditional sense, but the effect on your budget is the same.

The Low-Grade Fever Forecast

JPMorgan describes the situation as a "low-grade fever", not a full-blown crisis, but definitely not healthy. They're projecting inflation rising to around 3.5% by late 2025, then cooling to 2.8% by the end of 2026. That's still 40% higher than the Fed's target, and it assumes everything goes according to plan.

The truth is, we're in uncharted territory. We haven't had tariffs at this scale in recent history, we haven't had government spending this aggressive outside of wartime, and we haven't had this much uncertainty about what comes next. Anyone who tells you they know exactly what inflation will do is either lying or selling something.

What This Means for You

The gap between what the experts say and what you're experiencing isn't an accident, it's a feature of how the system measures inflation. The CPI was never designed to capture your personal inflation rate; it's designed to create an average across millions of people with different spending patterns.

But if you're a regular person spending a higher percentage of your income on rent, car insurance, and groceries, the very things that are most inflated, then your personal inflation rate is way higher than 2.4%. And that's the dirty secret they don't want you to focus on.

So yes, inflation is "under control" if you're looking at the government's carefully curated basket of goods. But if you're looking at your bank account, your credit card statement, and the anxiety you feel every time you need to fill up your tank or buy groceries, you know the real story.

The experts can say whatever they want. Your wallet tells the truth.

Be mindful, be watchful and good luck.