You ever feel like the economy is just one giant game of Jenga? One piece gets pulled out, the whole tower wobbles, and some guy in a suit at a podium, usually Jerome Powell, tells you it’s all part of the plan.

Well, welcome to April 2026. If you’ve been watching the news lately, you’ve heard the term “Fed Rate Cuts” more times than you’ve seen a political ad in an election year. But for the regular guy trying to figure out if he can afford a new truck or if he should keep his cash in a shoebox, the "Fed" can feel like a mysterious cult.

Let’s break it down. No PhD required. No boring spreadsheets. Just the facts, in under three minutes of reading (okay, maybe four if you read slow, but we're moving fast here).

The Fed is the Economy’s Thermostat

Think of the Federal Reserve as the guy in the office who is always messing with the thermostat. When the economy is "too hot" (inflation is high, everyone is spending money like they just won the lottery, and a gallon of milk costs as much as a streaming subscription), the Fed raises rates to cool things down.

When the economy is "too cold" (people are losing jobs, businesses aren't hiring, and the vibe is generally "ugh"), they cut rates to turn the heat back up.

Throughout 2024 and 2025, we saw the Fed pivot. After cranking rates up to a 23-year high back in 2023 to kill off that post-pandemic inflation monster, they finally started hitting the "cool" button. We’ve seen about 1.75% in cuts over the last two years.

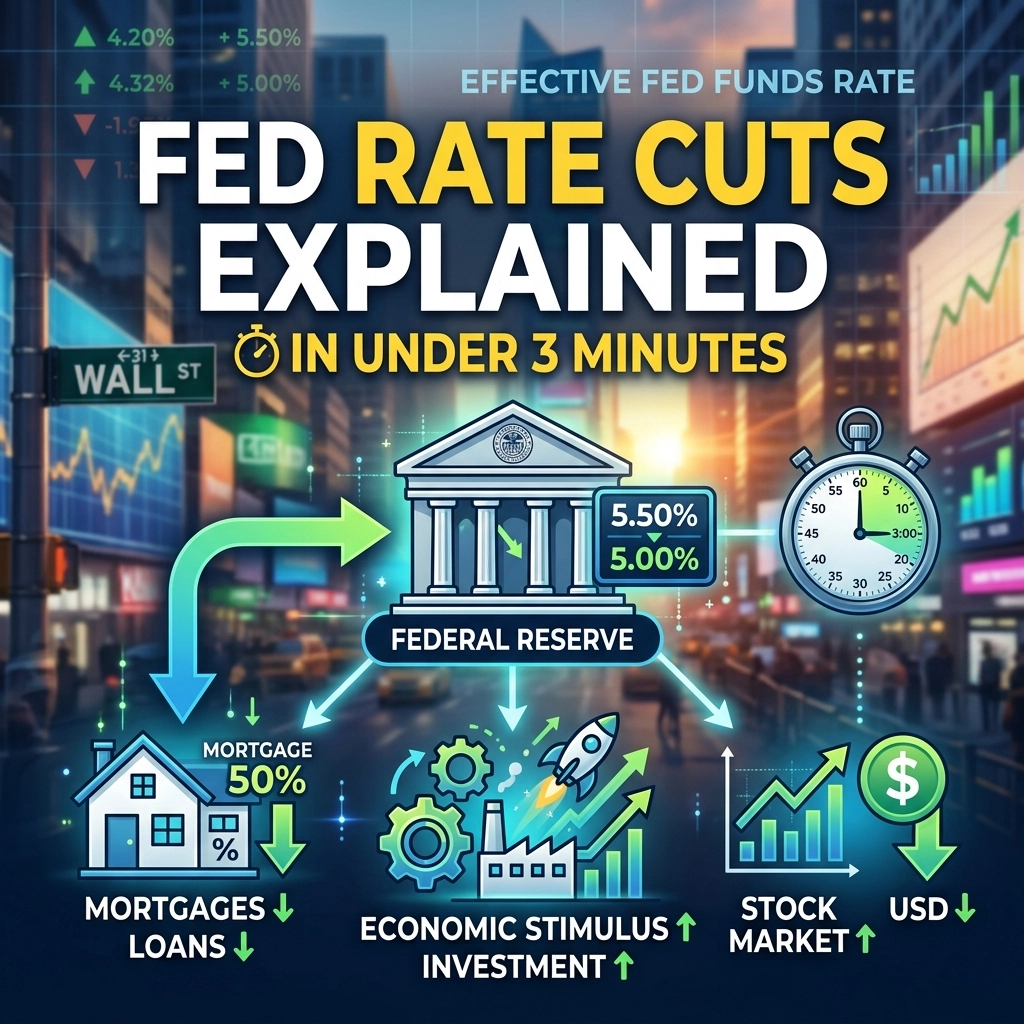

Why Should You Care? (The Borrowing Game)

When the Fed cuts the "benchmark rate," they aren't directly changing the price of your Netflix sub. They are changing how much it costs banks to borrow money. And because banks aren't exactly known for their charity, they pass those savings (or costs) down to you.

1. Mortgages: The 3% Dream

We all remember the glory days of 3% mortgages. Then we hit the 7% and 8% wall, which basically turned the housing market into a ghost town. When the Fed cuts rates, mortgage rates usually follow.

However, and this is a big "however", mortgage rates are like a moody teenager. They don’t always do what their parents (the Fed) tell them to do. They track things like the 10-year Treasury yield. So, even though the Fed has been cutting, you might see mortgage rates wiggle around. But generally speaking? A rate cut is the best news a homebuyer has had in years. It means your monthly payment might actually leave you enough room to buy groceries.

2. Credit Cards and Auto Loans

This is where you feel it fastest. Most credit cards have "variable rates." That’s a fancy way of saying your interest rate is tethered to the Fed’s movements. When the Fed cuts by 0.25%, your credit card interest usually drops by the same amount within a month or two.

If you’re carrying a balance (which, let’s be honest, most of us are), these rate cuts are a lifeline. It means more of your payment goes toward the actual pizza you bought three months ago and less goes into the bank’s pocket.

3. Car Loans

Thinking about that new Ford Lightning or a reliable Toyota? Rate cuts make auto loans cheaper. When rates were at their peak, a $40,000 car could cost you an extra $150 a month just in interest. With the recent cuts, that math is finally starting to look a little less like a horror movie.

The Bummer: Your Savings Account

Now, it’s not all sunshine and rainbows. There is a "Regular Guy" tax to rate cuts.

Remember those High-Yield Savings Accounts (HYSAs) that were actually paying you 4% or 5% back in 2024? Yeah, those are the first things to get hit when the Fed cuts rates. Banks are incredibly fast at lowering the interest they pay you, even if they’re slow at lowering the interest they charge you.

If you’ve got a big pile of cash sitting in a savings account, you’re going to see your monthly interest payment shrink. It’s the Fed’s way of saying, "Stop hording your cash and go buy something!" They want that money circulating in the economy, not sitting under your digital mattress.

The Big Picture: Capitalism and the "Runaway Train"

Here’s where we get into the "Regular Guy Economics" philosophy. Why is the Fed constantly fiddling with these numbers? Because our current version of capitalism is a runaway train of costs.

Take a look at the medical industry. In 1960, medical costs were 5% of our GDP. By 2025, they hit 20%. We are spending more money than ever, yet we aren't necessarily healthier. We've got more cancer, more diabetes, and more stress.

Just like medical costs have escaped the "noose" of common sense, the general cost of living has been on a tear. The Fed uses rate cuts as a tool to keep the engine from seizing up, but it’s a temporary fix for a systemic problem.

We see companies like Amazon, Berkshire Hathaway, and JPMorgan Chase trying to form their own healthcare companies to escape the "profit-making incentives" that drive costs through the roof. They realize that the traditional model is broken. The Fed’s interest rate maneuvers are a bit like that: they are trying to manage a system that is fundamentally designed to extract as much value as possible from every dollar you earn.

What You Should Do Right Now

So, the Fed is cutting rates. What’s the "Regular Guy" move?

- Refinance if you can: If you bought a house in 2023 or 2024, keep a very close eye on the rates. You might be able to shave a full percentage point off your mortgage soon, which adds up to tens of thousands of dollars over the life of the loan.

- Pay down the plastic: Use the slightly lower interest rates on your credit cards to attack the principal. Don't just celebrate the lower payment; use it to get out of the debt trap.

- Lock in those CDs: If you have extra cash, look into a Certificate of Deposit (CD) now. You can "lock in" today’s higher rates before the Fed cuts them even further.

- Invest in yourself: As we always say, the best hedge against a weird economy is being a healthy, productive human. Rate cuts make it cheaper for companies to expand, which usually means a better job market. Be ready to jump on opportunities.

The Bottom Line

Fed rate cuts are basically the government’s way of trying to make life a little more affordable without letting inflation spiral back out of control. It’s a delicate dance. If they cut too fast, prices skyrocket again. If they cut too slow, the economy crashes.

Right now, in April 2026, we are in the "soft landing" zone. Things are getting a bit cheaper to borrow, but the days of "free money" (0% interest) are likely gone for a long time.

We need to be smart. We need to look at our budgets the same way those big companies look at theirs: by optimizing every dollar and refusing to pay the "capitalism tax" where we don't have to. Whether it's negotiating a medical bill or shopping for a better mortgage rate, you have to be your own advocate.

The Fed is moving the chess pieces, but you’re the one playing the game.

Be mindful, be watchful and good luck.