If you’ve pulled up to a gas pump lately, you’ve probably felt that familiar sting in your wallet. We’re sitting at a national average of about $4.04 a gallon right now, and for the "regular guy," that isn't just a number on a screen, it’s a direct tax on getting to work, picking up the kids, and living life.

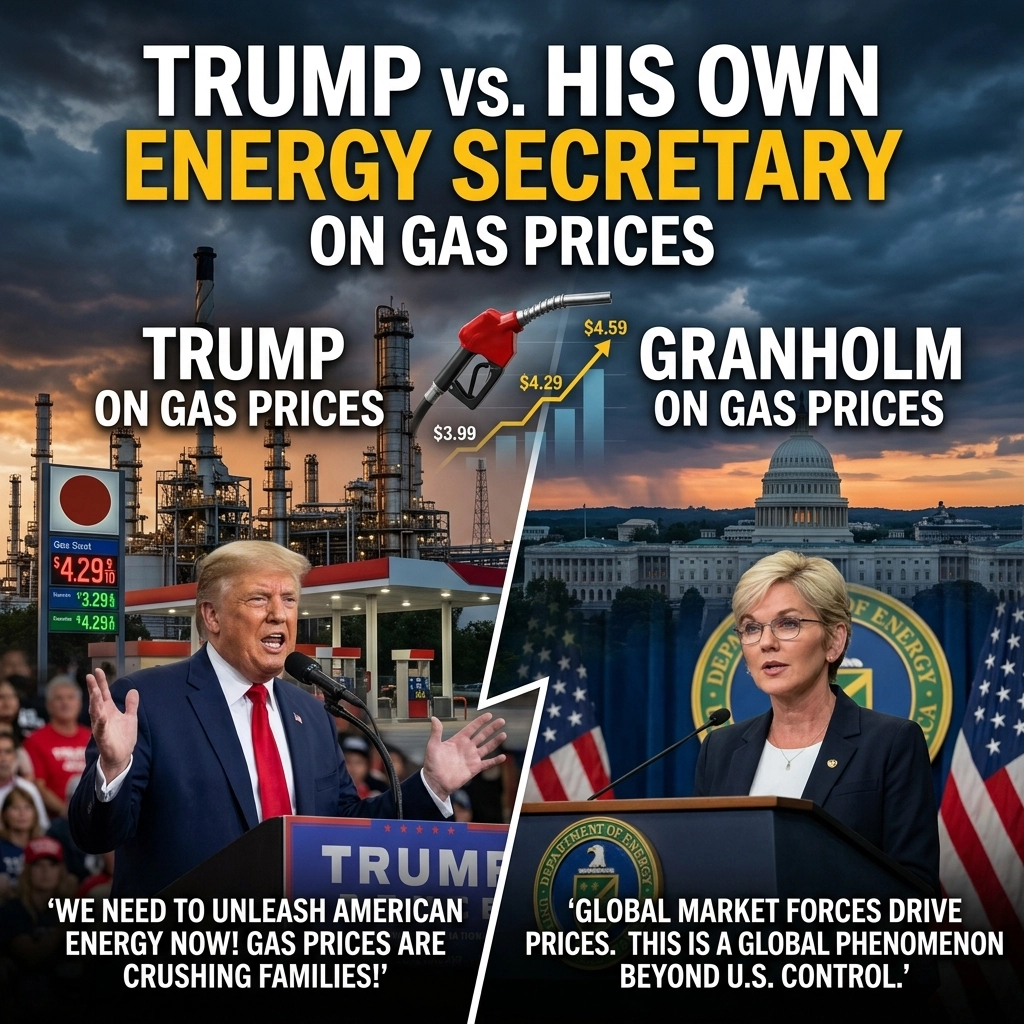

But this morning, things got a little weird in the world of high-level politics and energy policy. We had a classic "he said, he said" moment that leaves the rest of us scratching our heads and wondering who actually has their hand on the thermostat. On one side, you’ve got President Trump. On the other, you’ve got his own Energy Secretary, Jennifer Granholm.

They aren’t just disagreeing on the small stuff; they are living in two different timelines regarding when you’ll actually see relief at the pump. Let’s break down the drama and what it actually means for your bank account.

The Public Contradiction: A Tale of Two Timelines

Here’s the news peg from this morning’s CNN live blog: Energy Secretary Jennifer Granholm went on "State of the Union" and basically told Americans to buckle up. She said that while everyone wants gas prices to drop, the kind of big relief people are hoping for may not really show up until next year.

Wait, next year? For a regular guy trying to budget for a summer road trip in 2026, that feels like a lifetime away.

Naturally, President Trump wasn't about to let that "doom and gloom" forecast sit. In a phone interview with The Hill shortly after, he publicly checked his own guy. Trump’s take? "No, I think he's wrong on that. Totally wrong." Trump’s argument is that as soon as the conflict with Iran ends and the blockade of the Strait of Hormuz is lifted, the floodgates of oil will open and prices will plummet instantly.

So, who do you believe? The guy running the Department of Energy or the guy in the Oval Office?

Why the Strait of Hormuz Matters to Your Commute

To understand why they are fighting, you have to understand the "choke point." Right now, the global oil market is being held hostage by the situation in the Middle East. Iran has been making moves around the Strait of Hormuz, which is basically the world’s most important windpipe for oil.

About a fifth of the world’s total oil consumption passes through that narrow stretch of water. When things get heated there, insurance rates for tankers skyrocket, supply chains get jittery, and the "risk premium" gets tacked onto every gallon you buy in Ohio or Florida.

Trump’s logic is simple: End the war, open the Strait, and the oil flows. He sees it as a binary switch: on or off. When the blockade ends, Iran loses its leverage, and the market returns to "normal."

But Jennifer Granholm, the Energy Secretary, is looking at the plumbing. She knows that even if the "war" ends tomorrow morning, the economic ripples don't just vanish. We’re dealing with a "long tail" of inflation. Reopening trade routes, stabilizing global shipping, and getting production levels back to where they need to be takes time. Plus, $3.00 gas in 2026 isn't the same as $3.00 gas in 2019. Inflation has baked higher costs into the entire system: from the electricity that runs the refinery to the wages of the guy driving the tanker truck.

The Economics of "As Soon As This Ends"

Let’s talk about that "as soon as this ends" promise. In the world of Regular Guy Economics, we know that things rarely move as fast as politicians promise.

Markets are built on expectations. Right now, the market expects trouble. When the trouble ends, the market will breathe a sigh of relief, sure. But we also have to deal with the fact that our own Strategic Petroleum Reserve (SPR) has been a hot topic of debate. We’ve tapped into our reserves to keep prices from hitting $6 or $7, but those reserves eventually have to be refilled. When the government steps back into the market to buy millions of barrels of oil to refill those tanks, guess what happens to the price? It stays supported.

This is likely what Secretary Granholm is looking at. She sees the math of supply, demand, and the reality of refilling our "savings account" of oil. She sees a path to lower prices, but it’s a slow walk, not a sprint.

Trump, on the other hand, is playing the role of the ultimate optimist. He knows that high gas prices are a political killer. He needs the public to believe that relief is right around the corner. If the Energy Secretary says "2027," it sounds like the administration is giving up. Trump’s "totally wrong" comment is a signal to the markets and the voters that he intends to force those prices down much faster.

The "Broken Economy" Feeling

The reason this contradiction matters so much is that gas prices are the ultimate psychological barometer for the economy. You might not know what the S&P 500 did today, and you might not know the current yield on the 10-year Treasury note, but you know exactly what gas costs because it’s printed in six-foot-tall glowing numbers on every street corner.

When the President and his Energy Secretary can’t agree on the timeline, it adds to that "broken economy" feeling. It makes the regular guy feel like nobody is actually at the wheel. If the experts say one thing and the boss says another, who is actually making the policy?

We’ve seen this movie before. In the 1970s, energy policy was a mess of contradictions, and it led to years of stagflation: low growth and high prices. We aren't quite there yet, but the friction between "market reality" (Granholm’s view) and "political will" (Trump’s view) is where the sparks are flying.

What Should You Do?

So, what does this mean for your wallet?

First, don't bank on $2.50 gas by next month. Even if the war ended tonight, the logistics of the global energy market move like a freight train, not a Ferrari. Secretary Granholm’s next-year timeline might be a bit too pessimistic, but it’s grounded in the reality that inflation is a sticky beast.

Second, watch the Strait of Hormuz. That is the "news peg" that actually matters. If you see headlines about a "de-escalation" or the blockade being lifted, you can expect the prices at your local station to start drifting down within a few weeks. But as long as that "choke point" is under pressure, $4.00 gas is likely the new floor, not the ceiling.

Third, remember that energy is part of everything. It’s not just your car. It’s the cost of the plastic in your water bottle and the cost of the truck that delivered your groceries. High energy prices sustain high grocery prices.

At Regular Guy Economics, we like to look at the "spirit" of the market. Right now, the spirit is confused. When the top two guys in charge of energy are publicly calling each other "wrong," it tells us that there is no unified plan. It’s a "wait and see" mode, which usually means volatility.

If I told my wife the lawn would be mowed "as soon as this ends" while the lawnmower was clearly on fire in the driveway, she’d have some follow-up questions. That’s where we are with gas prices. The mower is on fire, and we’re arguing about how long it’ll take to cut the grass.

Final Thought

Whether it’s this year or next year, the era of "cheap" energy is under massive pressure. Between global wars, the push for green energy, and the depletion of our reserves, the regular guy is the one stuck holding the bill. Trump wants to be the hero who brings the price down instantly, while Granholm is trying to be the realist who manages expectations.

The truth, as always, is probably somewhere in the middle. We’ll likely see some relief if the war ends, but don't expect to go back to the "good old days" of 2019 prices anytime soon. The math just doesn't add up.

Be mindful, be watchful and good luck.